On Thursday, the Bank of England raised the base rate to 3%, the biggest single hike in 33 years – but is it really all doom and gloom…

This week we saw the 8th consecutive rise in the Bank of England base rate since December 2021 and as to be expected, there’s been a media frenzy of fear-mongering headlines and doomsday predictions wherever you dare to look.

Before we get into it, if you’re struggling to get your head around all this talk of interest rate rises – check out this article I wrote which goes into a bit more detail about the base rate, inflation and the relationship between the two;

Read Here – Interest Rates Rise Again, But What Does It Mean For You?

Essentially, by increasing the base rate it’s hoped that it will bring down “inflation” (the rate at which prices are increasing) because everything becomes more expensive and people have less disposable income to spend.

Then, in theory, because people are spending less, demand drops and prices stop rising so fast.

It’s thought that a little bit of inflation is good for an economy, but when prices are increasing too quickly buying power is reduced and the quality of living decreases – ironically, the exact strategy they’re using to try and kerb that same impact!

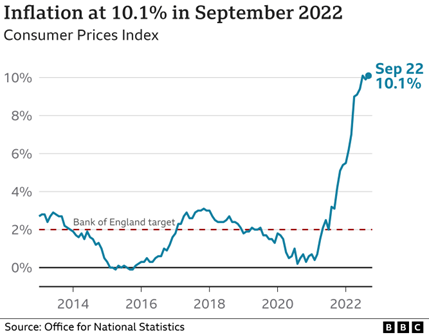

The target rate of inflation (the rate at which prices increase) for the Bank of England is 2%, and as you’ll see from the graph below, it’s recently shot up to over 10% – which is why they’ve decided to take action so soon after the last increase in September and raise it again;

So what impact does this have on the property market?

Raising the base rate makes borrowing more expensive.

Monthly repayments on a mortgage for the same property will now be higher than they were a couple of days ago because when the base rate increases, so do interest rates for new mortgages.

It also means that people who took out a “tracker mortgage” (a mortgage with an interest rate that is directly tied to the Bank of England base rate) or are coming to the end of their “fixed term” (an interest rate that is “fixed” for a given amount of time, for example two or five years) will now have to pay more than they have been.

In fact, it’s estimated that around 1.6 million people will find themselves with higher mortgage payments as a result of this latest rise.

Now, if you subscribe to the sentiment of the press, you’d be forgiven for thinking that it’s the end of the world and nobody is going to be able to afford to continue to live in their home.

But let’s add a little bit of perspective.

This .75% raise in the base rate means that the monthly increase on a typical tracker mortgage is going to be £73.50 a month and for those on a variable mortgage, £46.

Yes, it means that many of us may have to cut down on our expenditure to make sure we can keep on top of our mortgages, which nobody welcomes with open arms. Plus, it hits us in our pockets at a time when things are getting tough with rising energy costs etc. – but in isolation it’s an extra £2.45 a day or £1.50 per day depending on which type of mortgage you’re on.

Unwelcome, absolutely. But, perhaps not quite the unsurmountable rise in costs that the press would have you believe.

Also, does it mean that some people who perhaps could have afforded a property now can’t – perhaps.

But remember, interest rates have been at HISTORIC lows for over a decade so there was only ever one way they were going to go………….up.

How does it affect property prices?

Nobody can predict this with accuracy, despite how confident they might be in their guess (which essentially any prediction on property prices always is).

It was only a few days ago when it was predicted that the base rate would rise to over 6% by June 2023 and that prediction has now already dropped to 4.75% – things can change very quickly. Especially once the initial impact of a new headline passes and the dust settles.

And as my colleague, Emma Trowbridge at Hannells Oakwood, just reminded me – remember when everyone predicted the market would completely tank when COVID first hit….?

From our perspective at Hannells, it’s fair to say that property prices have been rising rapidly over the last couple of years and people have quickly gotten used this as a new “normal”.

For example, in June 2019, the average price of a UK property was £230,292.

In July 2022, that figure was £292,000, a difference of almost £62,000!

This rate of increase was always unsustainable and was going to come to an end at some point.

Let’s go back to 2019 (which was considered an active market).

House prices had grown just £16,000 over the previous three year period – compared to the £56,000 that we’ve just seen.

Given what we’re experiencing at the moment and have been for the last few weeks, we’d expect that property prices now start to plateau (as it usually does towards the end of the year) and then get back to a much more steady rate of increase next year (basically, what we’d have considered “normal” before the pandemic).

When you look back historically, property prices always increase over time and given that the UK is WAY under target for new homes being built, national demand will continue to outweigh supply for many years to come.

How does it affect the property market?

For every expert that tells you the market will crash, I’ll show you another expert – with access to exactly the same data – that will predict the opposite.

The property market since the return from COVID has been at an all-time high and due to a number of unique, influencing factors – this period HAS to be seen as an anomaly.

When you look back at the years before that, all of which were considered a busy and active market, we’re still seeing very similar levels of buyer and seller activity to then.

One example of this being that borrowing in September this year was actually HIGHER than the same month in 2016, 2017, 2018 and 2019!

Plus, during what’s widely considered as the last property “peak” back in 2006/07, it’s easy to forget that the Bank of England base rate was 5.5% and the average cost of a variable mortgage was 7.5% – and the market was doing pretty good back then!

True, that eventually came to an abrupt end but there are a huge number of mitigating circumstances back then which are very different now (such as the surge in repossessions, bank liquidity, irresponsible lending with little-to-no stress testing etc.)

It’s all too easy to soak up the clickbait news headlines and then subconsciously be looking for evidence to support them – which binds us to what’s really happening and makes everything seem much worse than it is.

There’s load of reasons and situations why people will always need to buy and sell property!

So, if I’m thinking of moving what should I do?

My advice here is the same no matter what month, year or type of market we’re in.

If you already own a property, book a valuation (you can do that with Hannells >> HERE <<) to find out how much yours is worth.

Then, speak to a mortgage adviser (we can help with that too!) to find out and clarify exactly what your financial position is.

If you can afford it and you find a property you want to buy – go for it!

If you can’t – don’t!

And that will always be the case.

Literally as I type this, Joe Thompson (one of our very own expert, in-house, mortgage advisers) is telling me about how he’s got emails coming in from lenders who are already DROPPING their rates – less than 24 hours after the announcement of the rise in the base rate. This goes back to what I was saying earlier about letting the dust settle.

Anyway, I hope this helps to bring things a bit more into context and help you to figure out what’s best for you.

After all, there’s no one-size-fits-all solution because all of our circumstances are so completely unique.

Just make sure you do your due diligence and get all the information to hand before you commit to making any decisions.

And if there’s anything we can do to help here at Hannells, feel free to get in touch and if there’s any questions I can help you with, send an email to ben.brain@hannells.co.uk

Regards

Benjamin

To catch all of our latest content, make sure you subscribe to our social media channels below!

Facebook: Facebook.com/Hannells

Instagram: Instagram/HannellsEstateAgents

Youtube: Hannells on Youtube

LinkedIn: linkedin.com/company/hannells-estate-agents

Hannells – A Moving Experience…