You might have heard in recent news headlines that the Bank Of England has raised it’s interest rate from 1.75% to 2.25%…

Although the rise is lower than many expected, it’s the seventh consecutive rise in the interest rate since December 2021.

But what does it actually mean and how does it affect you?

That’s what I’ll be attempting to break down in this article.

But first, let’s add a bit of context to the situation.

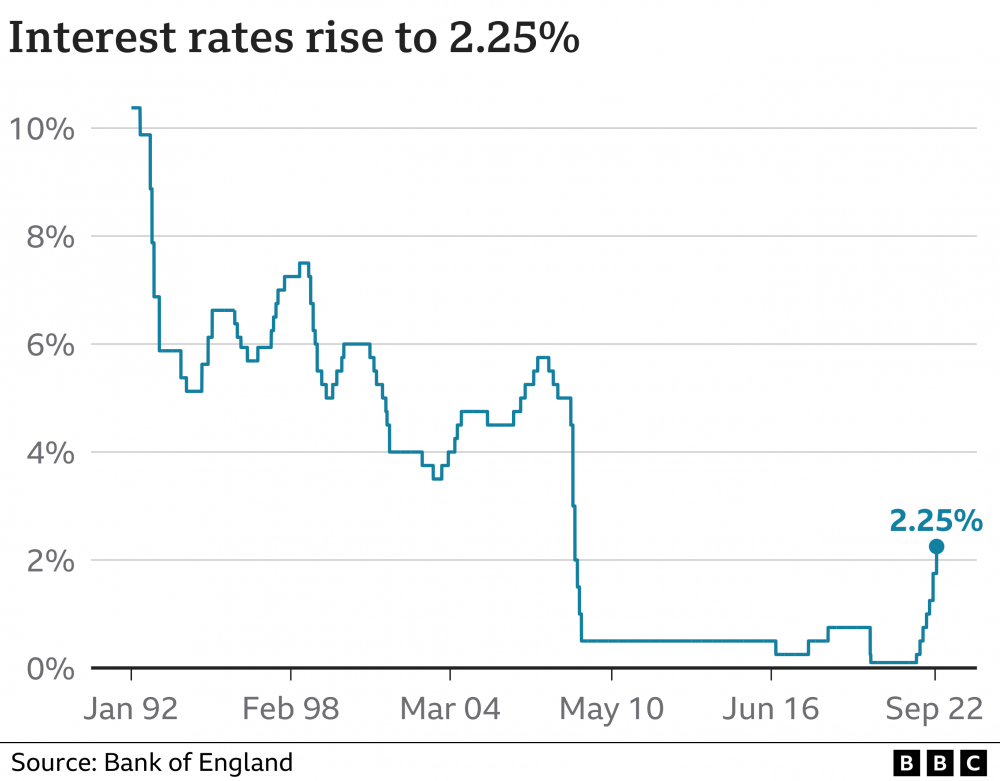

Despite this latest raise meaning the interest rate is the highest it’s been in 14 years, it’s still at an historic low.

Back in 2007, it reached as high 5.75%.

In fact, between the years of 2000 and 2008, it never dipped below 3.5% which you can see on the chart below;

So, whilst the interest rate will continue to creep up and is expected to be at 3% before the end of 2022 – it was always likely to happen since when anything reaches a record low, the only way is up.

Now you might be wondering – what exactly is the Bank of England Interest Rate and what’s the impact of changing it?

Well, essentially an interest rate tells you how high the cost of borrowing is, or how high the rewards are for saving.

The ‘Bank Rate’ is the key interest rate in the UK and it’s the job of the Bank Of England to set this interest rate.

It’s important because it influences many other interest rates in the economy. That includes the lending and savings rates offered by high street banks and building societies.

So, if the “Bank Rate” is 2.25%, why is the interest rate I pay on my mortgage more expensive?”

This is a great question.

Typically, a lender has to factor in more than the current “Bank Rate” when deciding on the interest rate you’ll be charged for your mortgage.

They need to factor in how “risky” you are as a borrower (i.e. how much of a deposit you have versus what you’ll be borrowing) and also add in the actual cost of them lending the money to you which includes things like staff and administration costs.

The mortgage rate you’re offered actually includes:

Bank Rate + Risk of customer + cost of actually lending the money = Your mortgage interest rate.

So, what’s the point of the Bank of England raising or reducing the Bank Rate?

Typically, the Bank Rate is used as a way to try and control inflation – which essentially means the rate at which things are increasing in cost.

Inflation isn’t always bad news. A little bit is actually quite healthy for an economy.

When the Bank Rate goes down, it’s usually because inflation is too low.

Interest rates go down which means it’s cheaper to borrow money and people are more confident to go out and spend.

This increases demand for goods and services, which can then lead to inflation.

The downside is that it means you earn less on your savings.

When the interest rate goes up, like we’re seeing at the moment, it’s usually in an attempt to dampen inflation, because it has the opposite effect.

It costs more to borrow money which means that people are encouraged to save more and spend less, which reduces the demand for good and services.

Essentially, the Bank Rate is used to try and control how people spend their money, how much it costs to borrow money and how much people save.

What makes getting this right difficult is that world events which are outside of our control can also have a significant impact on inflation – such as gas and energy prices which we’re seeing rocket up in price due to conflicts in other countries.

And finally, how does all of this affect the property market?

You’ve probably already guessed but a higher interest rate means that borrowing for a mortgage becomes more expensive.

As an example, let’s say you have a £130,000 mortgage that you want to pay off over 25 years.

If the interest rate on the mortgage is 2.5%, the monthly repayment will be £583.

If the interest rate on the mortgage is 3.5%, the monthly repayment would be £651 – a difference of £68 per month.

One example of how we’ve seen this affecting some buyers lately is that if they’ve not managed to find a property before their current mortgage offer expires, and there’s a rise in the rates – when they go to re-apply for the same mortgage, they may actually find that it’s no longer affordable for them.

Which means that in order to purchase the same property, the borrower must either pay more on their monthly payments, save for a larger deposit or adjust their budget to factor in the increased cost of lending and now look at properties in a lower price bracket.

And a change in the Bank Rate doesn’t just affect new mortgages.

If you have a fixed-rate mortgage – the interest is fixed for a set period of time. If interest rates change, generally during this period, it won’t affect your fixed rate or your monthly payments.

But bear in mind that if you don’t switch or re-mortgage when your fixed rate ends, you may be automatically moved onto your lender’s standard variable rate (SVR).

If you’re on a variable rate mortgage, or have a tracker mortgage, a change in the base rate – and interest rates – is likely to have an impact on your monthly payments.

Finally, the golden question, is now a good time to buy?

Well, that’s a tricky question to answer for everyone because it depends on your personal circumstances and whether you can comfortably afford to purchase the property that you want.

However, it’s worth bearing in mind that whilst borrowing has just become more expensive overnight because of the rate rise, it’s only going to continue to get more expensive with each subsequent increase.

Plus, the general consensus is that house price growth is going to continue (albeit at a slower rate than we’ve seen for the last 18 months) for the forseeable future.

So, hopefully you’ve now got a much better understanding of what’s actually going on when you hear about interest rate rises in the news and the reasons behind it.

I hope you found it useful and if you have any other questions, please feel free to send them over via email to me at ben.brain@hannells.co.uk.

Hannells – A Moving Experience