Inflation Drop Fuels Hopes of Interest Rate Cuts — What It Means for the UK Property Market

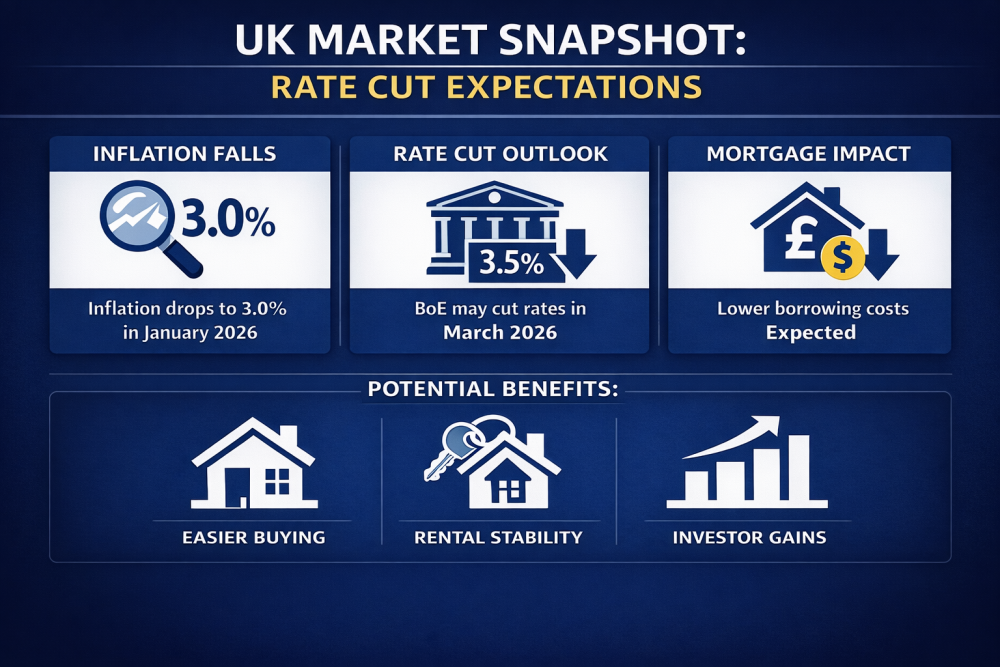

UK inflation slowed to 3.0% in January 2026, marking the lowest annual rate since March 2025, according to data released by the Office for National Statistics (ONS). This latest reading, down from 3.4% in December 2025, has sparked renewed expectations that the Bank of England (BoE) could cut interest rates as early as March 2026.

📉 Inflation Continues to Ease

The slowdown in inflation reflects broad price softening across key areas such as petrol, food and transport costs. While prices are still rising year on year, the pace of increase has eased significantly, strengthening confidence that inflation is steadily moving back toward the BoE’s long term target of 2%. Market pricing currently places a high probability on a base rate cut in March, with analysts suggesting the BoE could reduce its current 3.75% benchmark rate to 3.5% at its next Monetary Policy Committee meeting.

🏡 Impact on Mortgages and the Housing Market

Lower interest rates, if confirmed, would likely have a positive impact on mortgage costs. Many lenders base mortgage pricing on expectations for the BoE base rate, so even the anticipation of cuts has already started to feed into reduced rates on competitive products. Earlier data shows standard mortgage rates and fixed deals trending lower as lenders compete for business.

For prospective buyers, this could mean improved borrowing affordability, particularly for those looking to remortgage or take out a new mortgage in the months ahead. Reduced borrowing costs can widen the pool of possible buyers and support increased transaction activity, a welcome development after periods of subdued movement in the market.

🔑 What This Could Mean for Buyers, Renters and Investors

🔹 Buyers:

A falling base rate tends to ease mortgage costs over time — lowering monthly payments and improving affordability for first time buyers and home movers alike. Increased confidence in the market and falling borrowing costs can also encourage more sales activity and potentially support modest house price growth.

🔹 Tenants:

Tenants may not benefit directly from interest rate cuts, but indirect effects can help. If mortgage costs fall and more buyers enter the market, landlord demand may stabilise, easing upward pressure on rents. That said, rental demand and supply dynamics remain key drivers, so rental trends may still diverge by region.

🔹 Investors:

For property investors, a lower rate environment could reduce financing costs and enhance returns, especially for those leveraged through buy to let mortgages. Lower interest costs may also support stronger capital growth if buyer demand rises. However, investors should consider broader economic signals, such as wage growth, unemployment trends and long term housing supply, when evaluating opportunities.

📈 Looking Ahead

While the 3% inflation figure is a positive sign, it remains above the BoE’s 2% objective — meaning policymakers will proceed cautiously. Still, as price pressures ease and borrowing becomes potentially cheaper, key indicators suggest easing financial pressure for households and a more supportive backdrop for property market activity throughout 2026.

If you would like tailored advice about buying, selling, mortgages or investing locally, get in touch with your nearest Hannells branch or arrange a free, no-obligation property valuation today.

If you would like tailored advice about buying, selling, mortgages or investing locally, get in touch with your nearest Hannells branch or arrange a free, no-obligation property valuation today.

Click HERE to book your free, no-obligation valuation.

Get in touch with your local branch of Hannells by clicking HERE

To catch all of our latest content, make sure you subscribe to our social media channels below!

Facebook: Facebook.com/Hannells

Instagram: Instagram/HannellsEstateAgents

Youtube: Hannells on Youtube

LinkedIn: linkedin.com/company/hannells-estate-agents

Hannells – A Moving Experience…

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE